📖 Top 10 China's AI Stories in 2024: A Year-End Review

Thanks to everyone who subscribed and read my stories this year!

Last week, my mom, 58, won a local dancing competition and was asked to give an award speech. Normally, this kind of task would fall on me – just as many others do. But this time, she told me she’d figured it out using an AI app. “The AI wrote it better than you ever could,” she said, implying that she might not need my help anymore.

In 2024, keeping up with AI’s rapid development in China has been a challenge. There are endless stories to tell – from frontier models to real-world applications. Every company is eager to sprinkle a bit of AI magic into its narrative.

As a long-time observer of China’s AI, the biggest theme in 2024 in my view is how quickly the nation is catching up with the U.S. In 2023, Baidu’s ERNIE 4.0 was the lone model claiming GPT-4-level performance. Fast forward to 2024, and there are at least five contenders – including Alibaba’s Qwen and DeepSeek – that have reached (though not yet surpassed) similar benchmarks. Earlier this year, Sora’s surprise release made waves, but just 10 months later, companies like Kuaishou and MiniMax are competing in the same battlefield with their video generators. Baidu’s ERNIE LLM API, for instance, is now used 1.5 billion times per day – a 30-fold increase over last year. Meanwhile, ByteDance’s Doubao LLM handles an impressive 4 trillion tokens every day. Beyond generative models, innovations in robotics and autonomous driving are transitioning from prototypes to large-scale implementation.

Yet 2024 wasn’t just about AI advances. China’s approach to AI safety evolved rapidly, U.S.-China dynamics remained complex, and industries grappled with AI’s ethical and societal implications.

As we close out the year, I want to wrap up with 10 AI stories that shaped 2024. Although these stories don’t capture the entire landscape of China’s AI progress, they highlight what I believe were the most significant developments. If there’s something you think deserves a mention, feel free to share your thoughts.

Finally, thank you for reading my newsletters. May the joys of the holiday season fill your heart and carry into the new year. Wishing you and your family happy holidays and a wonderful year ahead! 🎊🎈

The Hunt for AI Killer Apps

Over the past decade, as mobile internet rose, China became a hub for super apps like WeChat and TikTok. Now, with the generative AI revolution underway, the question looms: can Chinese companies deliver truly AI-native apps?

In 2024, several popular AI-powered apps are already making waves. Domestically, ByteDance’s Doubao has emerged as the hottest AI chatbot app, boasting 51 million monthly active users. Despite Doubao not being regarded the most advanced LLM in China, its popularity is credited to smart app design and effective user acquisitions. Following Doubao are Baidu’s ERNIE Bot (Wenxiaoyan for mobile) and Moonshot’s Kimi.

Internationally, Talkie, developed by MiniMax, ranks among the most downloaded AI apps in the U.S. It attracts young-age users to engage in conversations with LLM-powered virtual characters. Other AI apps made by Chinese companies making their mark include Question.ai from Zuoyebang, an AI-powered homework assistant, and Gauth, a similar tool from ByteDance.

“In China, we take a more application-driven approach,” said Baidu CEO Robin Li at an event in France this May discussing how China’s AI development differs from the West’s.

However, despite these advances, China has yet to produce an AI-native “killer app” – an app with at least 100 million daily active users in my definition. For comparison, OpenAI’s ChatGPT reportedly reached 300 million weekly active users by December. “China is still waiting for its ChatGPT moment,” said Kai-Fu Lee.

Opinions differ on what’s holding back the development of a super AI app. Some argue that patience is key, as inference costs will continue to drop and models will grow more capable in reasoning. Others question whether chatbots – mainly text-based interfaces – are the ideal format for the next killer app. Metrics like user retention and time spent remain lower for chatbots than for other mobile apps like TikTok, Instagram, or even Google.

Mixed Reality of AI Startups

Since ChatGPT’s debut in November 2022, Chinese entrepreneurs have been racing to create the country’s answer to OpenAI. Backed by massive capital from high-profile investors such as Hongshan (formerly Sequoia China), Hillhouse Capital, and tech giants like Alibaba and Tencent, four (or some say six) Chinese startups have emerged. These companies are:

Zhipu AI: Founded in 2019 by Tsinghua University researchers, Zhipu AI has strong academic roots. It has developed a family of advanced models in language, vision understanding, coding, and agents under its GLM series. Zhipu AI has raised RMB 3 billion ($412 million) in its latest funding round and valued at RMB 20 billion in September.

MiniMax: Founded in 2021 by former SenseTime executives, MiniMax developed one of the most-downloaded AI apps in the U.S., Talkie. Its valuation is over $2.5 billion as of March 2024.

Moonshot: Founded in 2023 by Yang Zhilin, Moonshot is known for its Kimi chatbot. Its valuation reached $3.3 billion in August 2024 after a Series B funding round where the company secured over $300 million from Tencent and Alibaba.

Baichuan AI: Founded in 2023 by former Sogou CEO Wang Xiaochuan, Baichuan AI focuses on AI in healthcare. The company raised RMB 5 billion ($687.6 million) in a funding round in July 2024 at a valuation of RMB 20 billion (~$2.8 billion).

Other two contenders include 01.AI, founded by renowned computer scientist Lee Kai-Fu, and StepFun, founded by former Microsoft VP Jiang Daxin. The latter just raised hundreds of millions of dollars, though its valuation remains undisclosed.

Startups often thrive during technological paradigm shifts. They can quickly adopt modern tech stacks without being burdened by legacy systems, target underserved niches that are overlooked by tech giants, and attract innovative talents.

However, Chinese AI startups now face a unique challenge: Tech giants are rapidly committing resources to AI and leveling the playing field. They have access to massive computing power, larger amount of data, and established applications.

As of now, only Moonshot’s Kimi has made it to the top three chatbots in China. Some startups, such as Baichuan and 01.AI, are seeing their co-founders leaving. Two unnamed startups have also reportedly halted their LLM pre-training.

China’s once ambitious “four small dragons” – led by SenseTime and Megvii – also face significant challenges today. SenseTime recently underwent a major restructuring to focus on generative AI, while Megvii abandoned its IPO plans amid losses of RMB 15 billion over three and a half years.

The current AI wave presents an opportunity for Chinese startups to rise again. With fierce competition from tech giants, only time will tell if these new contenders can achieve lasting success.

Growing Influence of Chinese Open LLMs

Chinese open-source LLMs have made remarkable strides globally in 2024.

Leading the charge is Alibaba’s Qwen model series. Its latest iteration, Qwen 2.5, has become the most downloaded open model on Hugging Face in 2024. Their latest offerings include QwQ for reasoning and QvQ for visual reasoning. Alibaba has incentives to prioritize open-source development as the company hopes it would drive a broader adoption of their cloud services.

Another notable player is DeepSeek, an AI lab backed by one of the largest quantitative funds in China, High-Flyer. DeepSeek has developed a suite of advanced models, including the R1 reasoning model and the V2.5 vision-language model, which have significantly closed the performance gap with leading closed models like Anthropic’s Claude-3.5 and OpenAI’s GPT-4o and o1. Their latest model, DeepSeek-V3, a 671B MoE open model, robustly outperforms Llama-3.1 but costs less than $6 million for pre-training.

Chinese open-source LLMs are also more accessible. For instance, MiniCPM is a lightweight open-source model developed by Tsinghua University in collaboration with AI firm ModelBest. In early June, three Stanford University students were accused of plagiarizing its multimodal model. MiniCPM has earned recognition for releasing model weights, training checkpoints, and public datasets. It also imposes no restrictions on commercial use.

Early Wins of AI Video Generators

The delayed release of Sora, OpenAI’s AI video model, created a 10-month window of opportunity for Chinese AI video generators to surge ahead globally. Platforms like Kuaishou’s Kling, MiniMax’s Hailuo, and Shengshu Tech’s Vidu have introduced innovative features, including multi-frame editing and stylized animations, while attracting users with competitive pricing and free trials. With these advancements, Sora now faces stiff competition.

Kling, announced in June, has attracted over 6 million users as of December, who have collectively generated more than 65 million videos and 175 million images. The model is good at simulating dynamic motions and natural environments, as well as image-to-video generation.

Meanwhile, Vidu, announced in April by Baidu-backed Shengshu Tech, can produce 5-second video clips in under 30 seconds. MiniMax, known for its Hailuo AI video model, plans to integrate it into Talkie, which directly competes with Character AI. Tencent also open-sourced its video generation HunyuanVideo, which features 13 billion parameters.

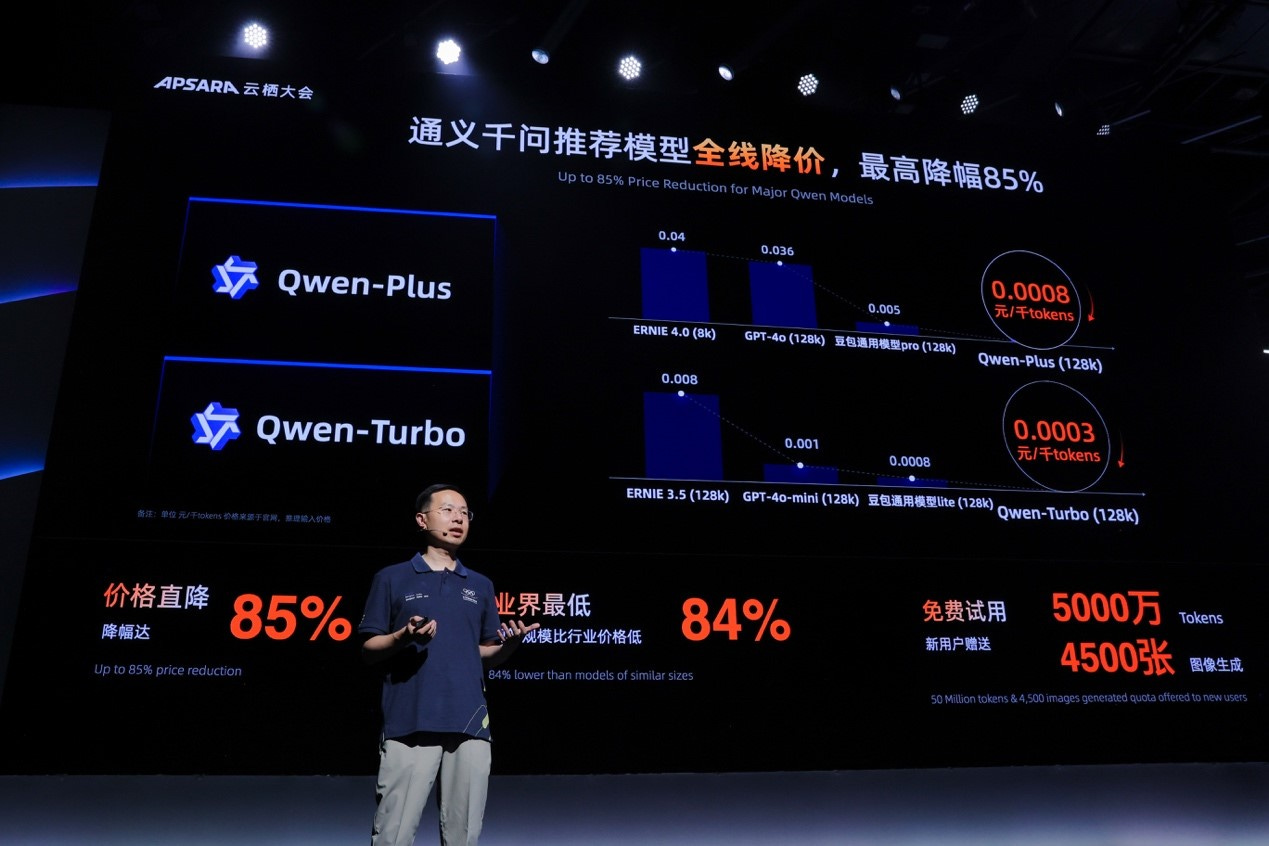

LLM API Price War

In May, major Chinese tech companies like Alibaba, Baidu, and ByteDance slashed prices on their LLM APIs, igniting an earlier-than-expected price war of LLMs. LLM APIs, which enable developers to integrate AI language processing into their applications, are typically priced per million tokens, with recent reductions marking a significant shift.

The price war began when DeepSeek introduced its LLM, DeepSeek-V2, at only RMB 1 (~$0.14) per million input tokens. Shortly after, Zhipu AI slashed its GLM-3-turbo API price by 80%, matching DeepSeek’s rate and increasing free tokens to 25 million.

Following this, ByteDance reduced the price of its Doubao model to RMB 0.8 ($0.11) per million tokens. Alibaba Cloud set the price for its Qwen-Long API at RMB 0.5 ($0.07) for input and RMB 2 (~$0.28) for output per million tokens – roughly 1/400th of the then GPT-4’s cost. On the same day, Baidu made its ERNIE Speed and ERNIE Lite APIs completely free. Tencent also joined the fray, offering free access to its Hunyuan-lite model and cutting prices for premium options.

The price war recently intensified when ByteDance introduced its Doubao Vision Understanding Model, pricing it at 1,000 tokens for 0.003 yuan ($0.0004). This means for one yuan ($0.14), the model can process 284 images at 720P resolution.

The inference cost of LLMs is decreasing significantly – by a factor of 10 each year – due to improved computational efficiencies, optimized algorithms especially model compression techniques, and economics of scaling. The price war is great news for developers and SMEs experimenting with AI, potentially accelerating adoption.

Chip Self-Reliance Amid Challenges

China’s semiconductor industry faced a tumultuous year in 2024. Investments in China’s chip industry dropped 35.9% year-over-year in the first 11 months, reflecting heightened US restrictions and concerns about overcapacity in legacy chip production. The U.S. again tightened export controls in October by blacklisting 140 Chinese companies and restricting access to high-bandwidth chips essential for AI and advanced chipmaking equipment.

Despite these headwinds, China’s semiconductor production capacity is set to grow by 40% over the next five years, driven by the expansion of 12-inch wafer fabs. Meanwhile, companies like Huawei continued to push forward on self-sufficiency and competitive AI chips. The telecomm giant plans to mass-produce its Ascend 910C AI chip by early 2025, claiming performance on par with Nvidia’s H100. The company also introduced Harmony Intelligence that deeply integrates AI technology into its HarmonyOS for devices.

However, Huawei continues to face challenges scaling its chip production, particularly achieving high yields under U.S. restrictions. In October, TSMC discovered that chips – allegedly the Ascend 910B – it had manufactured for a customer were being used in Huawei products, potentially violating U.S. sanctions. TSMC suspended shipments to the suspected client, Sophgo, mid-month after identifying the connection to Huawei. Sophgo, an affiliate of bitcoin mining equipment supplier Bitmain, denied any direct or indirect relationship with Huawei, but the U.S. government is now considering adding the company to its blacklist.

Self-Driving Cars Gain Momentum

In 2024, China’s robotaxi industry, once teetering on lukewarm prospects, began proving that its business could grow and rival Didi Chuxing. Apollo Go, Baidu’s driverless ride-hailing service, now operates over 400 self-driving robotaxis in Wuhan, with plans to expand its fleet to 1,000 by year-end. The service logged nearly 1 million orders in Q3 and went viral on Chinese social media in July. It sparked excitement over the futuristic experience for urban transport – alongside growing discussions about its potential impact on traditional jobs.

Meanwhile, leading Chinese self-driving startups Pony.ai and WeRide completed their long-anticipated IPOs on Nasdaq, raising a combined $853.9 million. Pony.ai aims to grow its robotaxi fleet from 250 vehicles to over 1,000 by 2025. WeRide, meanwhile, partnered with Uber to bring autonomous vehicles to its platform, starting in Abu Dhabi, United Arab Emirates.

Chinese self-driving firms are also actively pursing global expansion, targeting markets in Southeast Asia and the Middle East through partnerships and localized deployments.

However, these advancements also come amid U.S.-China dynamics. In September 2024, the U.S. Department of Commerce proposed regulations to restrict the sale or import of connected vehicles, along with associated hardware and software linked to China and Russia. This move could pose significant challenges for Chinese autonomous vehicle companies seeking to expand into the U.S. market.

OpenAI, Microsoft Tighten AI Access to China

In 2024, OpenAI and Microsoft tightened restrictions on developer access to their AI services in China.

On July 9, 2024, OpenAI banned API access to its AI models in China, citing unauthorized traffic from unsupported regions. The move prompted swift reactions from Chinese AI leaders, including Baidu, Alibaba, Zhipu AI, and SenseTime, who announced seamless migration services and free tokens for OpenAI API users on the same day.

China has never been officially supported by OpenAI for API services. However, developers and enterprises in the region have relied on overseas proxy servers or Microsoft Azure to access GPT models, so that they can build products, services, and train models.

On October 21, 2024, Microsoft also terminated the Azure OpenAI service for individual developers in mainland China, citing compliance with local regulatory requirements. Enterprise customers in China can still retain access to the Azure OpenAI Service.

More recently, some developers have reported suspended accounts on Anthropic’s Claude, adding to concerns over access restrictions.

Some experts worry this could mark the beginning of a broader U.S.-China AI decoupling, with OpenAI under pressure to align with U.S. interests. This will accelerate China’s efforts to develop homegrown AI models.

Robotics Boom: From Prototype to Production

China’s robotics innovation, from humanoid to four-legged wheeled robots, is accelerating at an unprecedented pace.

One standout is AgiBot, a Chinese AI and robot company founded by Peng Zhihui, a former recruit from Huawei’s prestigious “Genius Youth” program. AgiBot this year launched a robot capable of intricate tasks like threading a needle.

Meanwhile, Unitree, often referred to as “China’s Boston Dynamics,” unveiled a robot capable of performing the Thomas Flare gymnastic move and leaping from a 2.8-meter rooftop. Adding to the list, UBTech’s Walker S humanoids are already assisting with assembly line tasks in BYD factories

The 2024 World Robot Conference, held in Beijing this August, also reflected the nation’s robotics boom. Featuring 169 exhibitors and over 600 products, the event unveiled 60 new robot models, with humanoid displays tripling compared to the previous year.

China’s robot industry has seen a meteoric rise in investment, with funding increasing from RMB 1.98 billion ($279 million) in 2019 to RMB 9.74 billion ($1.37 billion) in 2023.

Despite these innovations, many robots still struggle with complex, general-purpose tasks, while high production costs make them impractical for widespread use. Experts also debate the necessity of advanced features like dexterous hands, as many applications do not require such capabilities.

AI Resurrection: Healing Hearts or Crossing Ethical Lines

Resurrecting the deceased through computer-generated imagery is not a new concept, but the rise of generative AI – particularly diffusion models combined with LLMs – has made it remarkably simple.

Earlier this year, a deepfake video of Coco Lee, a renowned Chinese-American singer who voiced Disney’s Mulan and tragically died by suicide last year, went viral on Chinese social media. Created by a blogger claiming to fulfill fan requests, the video portrays Lee warmly engaging with her fans. One video only charges RMB 588 (~$82).

Meanwhile, some individuals use similar deepfake technology for personal healing. Musician Bao Xiaobo, for instance, created a digital version of his late daughter and sang a birthday duet with her.

Companies like China’s Silicon Intelligence have gone further, offering personalized services for grieving families. For example, Sun Kai, a co-founder of the company, created a digital replica of his mother after her sudden death in 2019. By providing photos and voice recordings, Sun enabled AI to replicate his mother’s likeness and speech. While the avatar initially had limited conversational abilities, Sun found solace in being able to “talk” to her.

The demand for these services is growing. Silicon Intelligence and similar companies now offer digital resurrection at increasingly affordable rates, with prices dropping from thousands of dollars to just a few hundred. This affordability, combined with improving technology, is making AI resurrection accessible to the masses.

Resurrection could open Pandora’s box of opportunities and challenges in the age of generative AI. On one hand, these tools offer comfort to grieving families, fostering connections that might otherwise feel lost forever. On the other, they pose significant ethical and legal dilemmas.

The most interesting AI wrap I've seen this year. Cheers from NZ...